.png?width=190&height=55&name=MPA%20Logo%20Vector%20-%20Original%20(3).png "Miller Public Adjusters")

Hiring a public adjuster for insurance claims helps you protect your payout. It also avoids costly mistakes an...

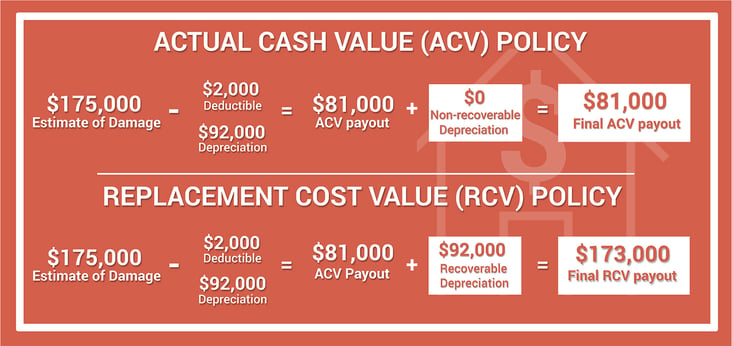

Most property insurance policies pay for damages, first, on an Actual Cash Value (ACV) basis. This means you receive payment for the replacement value of your damaged property — that is, the cost to replace what was damaged with new property of like kind and quality — less depreciation.

Of course, defining depreciation is more art than science. Your insurance company’s claims adjuster uses standard depreciation tables that reduce valuation of personal property by a given percentage each year. These tables do not take into account how your property was used, cared for, etc. For example, a $5,000 leather sofa in a formal living room that no one uses should not depreciate at the same rate as a discount store futon used in a playroom.

Negotiating fair ACV valuation requires a detailed inventory, a proper determination of which items were damaged vs. destroyed, and exhaustive research.

If you have Replacement Cost Value (RCV) coverage, once you replace your damaged property, you submit your receipts for reimbursement of the difference between the ACV payment you received and what you paid to replace your property with new property of like kind and quality. Always be sure to save all your receipts for any purchases related to your claim.

ACV and RCV are areas where policyholders are routinely underpaid for their damages. Some reasons for this include:

Some policies split the ACV/RCV hairs even thinner with provisions like, “functional replacement cost,” which means your repairs are covered only to the extent that the replacement functions as intended. For example, if your hardwood floors are water damaged, you could be compensated for the cost of laminate as a functional replacement. To replace your floors with hardwood would require you to pay the difference out of pocket.

At the other end of the spectrum is “guaranteed replacement cost,” which pays to replace damaged property at RCV, even if the total cost exceeds the policy limit.

The various types of ACV and RCV coverage illustrate just some of the many differences in policy language. These differences are why it’s so important to understand the provisions in your policy.