.png "Miller Public Adjusters")

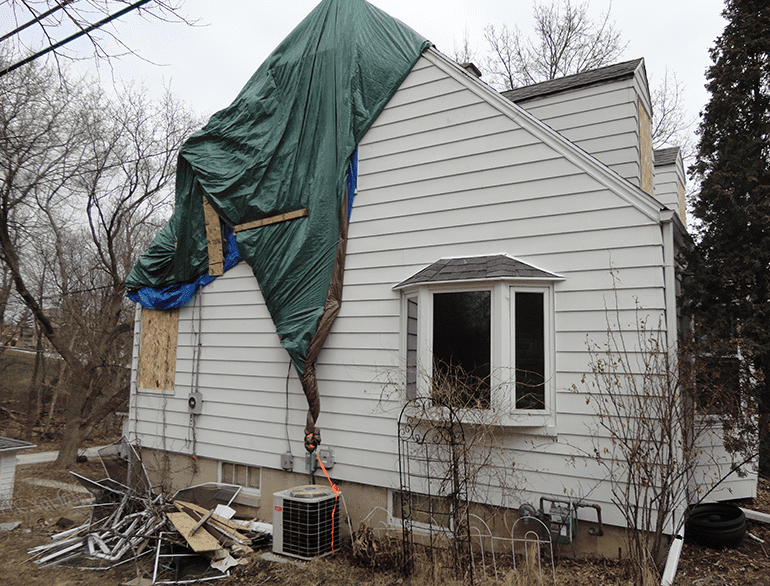

For years, you’ve dutifully paid the premiums on your homeowner’s insurance, hoping you'll never need to make a claim. Then a disaster strikes. Your home is flooded, a storm takes off your gutters and roof, or a fire wipes out your kitchen. You file a claim, never expecting to hear that your insurance policy won’t cover the damage. Unfortunately, that is exactly what many homeowners are told.

For years, you’ve dutifully paid the premiums on your homeowner’s insurance, hoping you'll never need to make a claim. Then a disaster strikes. Your home is flooded, a storm takes off your gutters and roof, or a fire wipes out your kitchen. You file a claim, never expecting to hear that your insurance policy won’t cover the damage. Unfortunately, that is exactly what many homeowners are told.

It’s disappointing when your insurer won’t pay, or the company makes a lowball offer on your claim that doesn’t begin to cover your losses, but there are steps you can take to correct this problem.

Smart Strategies

Good claim service by your insurer includes handling your claim promptly and fairly. A conflict may arise when your insurance company’s adjuster does not agree with your estimated losses and looks for ways to exclude some or all of them. While you may feel consistent payment of your premiums equals fair reimbursement at a time of loss, sadly it is not always the case. Making the decision to hire an expert to help you get what you’re entitled to may end up being your best defense. In the meantime, here are five ways you can avoid home insurance claim delays and get your insurance company to agree to your estimate.

- Work From a Common “Scope of Loss”

Typically more detailed that an estimate, a scope of loss describes the amount and type of damage that has been done to your home. It also includes the amount and quality of materials that will be needed to repair or rebuild your home, as well as the current cost of materials and labor. A clear scope of loss should help you eliminate lowballing and claim denials.

- Provide Comprehensive Details

Detailed descriptions, photographs, receipts, and diagrams are all key to a good scope of loss. The more detailed the information you can supply to your insurer, the better. In addition to the items already mentioned, look for blueprints or plans, drawings, appraisals and other real estate documents or videos. Don’t forget to document and photograph all damage.

- Proof of Expenses

Keep every receipt and financial document that you receive relating to your loss, including the cost of materials, labor and delivery. Submit them to your insurer along with the calculations of your total expenses. Seeing proof in black and white often results in the insurer adjusting what is often a computerized offer to accommodate your true costs.

- Ask Questions

Ask your adjuster plenty of questions like “how was the estimate calculated?” And “what costs went into the calculation?” Asking the right questions will let the insurer know you are serious about getting a fair and reasonable settlement.

- Avoid Being Pressured

Never sign a release until you are satisfied with the results of your claim. Insurance companies often have releases that can deny you coverages you never knew you had, so don’t let the insurer's adjuster pressure you into accepting an offer. You have more leverage than the insurance company wants you to know - they want to keep your business.

Bad Faith Insurance

Finally, when you buy insurance, you pay for both coverage and good service. If your insurance company denies your legitimate homeowner’s claim, you may be the victim of insurance bad faith, in which case you may be able to recover additional damages. Denial of coverage can result in a huge financial loss, so don’t let a bad faith action rob you of a fair settlement. Consult an expert about your rights.

Miller Public Adjusters currently serves the states of

Wisconsin -Florida - Illinois - Indiana - Michigan - Minnesota - Texas

Call us 24 hours a day at (866)779-8901 to schedule an appointment or

please fill out a Free Claim Review to see if we can help.