.png "Miller Public Adjusters")

Your comfortable life can get mighty uncomfortable when your home is damaged by fire, windstorm or some other catastrophe. Restoring your property and replacing your personal belongings can be an exhausting process. You might reasonably believe that your Homeowners insurance company should help you through the struggle; but when your insurance won't pay you what's fair, you might be forced to fight for the money you deserve.

Unfortunately, insurance companies don't always handle claims in good faith. Your insurance adjuster might be more concerned with pleasing his boss, keeping his average paid claims low, and closing his file. When your adjuster doesn't have your interests at heart, you must be prepared to fight for a fair settlement.

Fight for the money you deserve

The best way to prepare for your claim battle is to document your damages and review your Homeowners policy for a clear understanding of what is and isn’t covered. Your fight won't be solely over your contractor's estimate. Insurance disputes often shift into high gear when they involve obscure policy benefits, supplemental coverages and other issues you might not have anticipated. Here are a few to consider.

Depreciation

Most Homeowners policies pay for damaged contents on an actual cash value basis. Your adjuster will calculate ACV with the help of a depreciation table that lists average life expectancies for common items. For example, if your 7-year-old television has a 10-year life expectancy, the adjuster would pay you 30 percent of its replacement cost value. If your TV was in “like new” condition, you’ll have to fight for a better settlement.

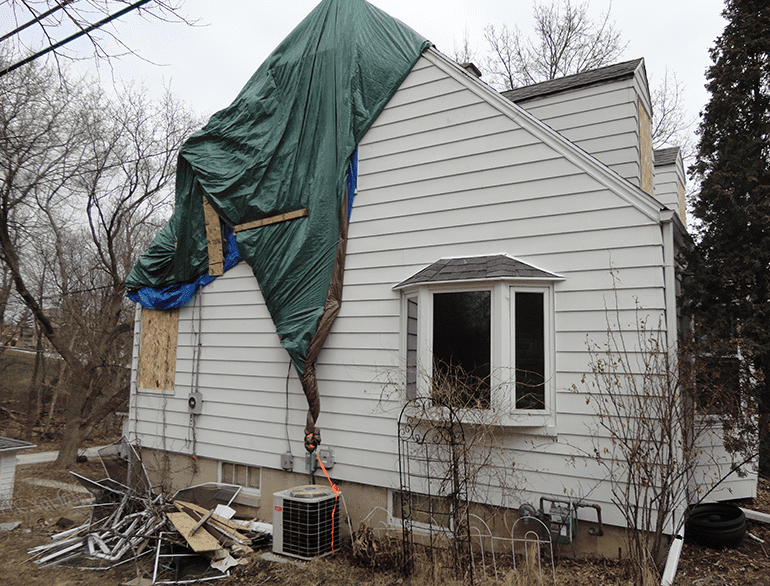

Water damage

Water damage often triggers an automatic “not covered-deny claim” response from an adjuster. He might be right, but water damage claims can be covered under very specific circumstances, such as “...accidental discharge or overflow…” from certain systems in your home. Water damage can also be covered when building damage initiates a chain of events that causes an influx of water. It's up to you to push your adjuster to get his facts straight.

Repair vs Replacement

The Section I, C. Loss Settlement provision of your policy explains options for repairing and replacing your damaged property. Repair vs replacement is usually the adjuster’s call, so if you prefer one option over the other, you will have to speak up for what you want.

Lightning damage to trees

When your tree is damaged by lightning during a storm, you are entitled to reimbursement. If the physical evidence doesn’t fit the adjusters perception of what lightning damage looks like, he may say it was wind (not covered) that caused the damage. It's up to you to prove him wrong.

Additional Living Expenses

When your home is damaged by a covered peril and you must relocate during the repair process, your policy pays your temporary living expenses. While the adjuster might push you to stay in the cheapest available accommodations, you are entitled to a temporary residence and services equivalent to your “...normal standard of living.”

A Public Adjuster can help

When your insurance adjuster won't pay what's fair, it could be a result of a nagging boss, a low reserve, or an incomplete understanding of policy coverages. No matter what causes your dispute, if you don't want to battle over your damaged home or business, a public adjuster can do it for you.

With no fees upfront, Miller Public Adjusters will take on your insurance company, fight your claim battles, and maximize your settlement.

Miller Public Adjusters currently serves the states of

Wisconsin - Florida - Illinois - Indiana - Michigan - Minnesota - Texas

Call us 24 hours a day at (800)958-4829 to schedule an appointment or

please fill out a Free Claim Review to see if we can help.